This blog is about data analytics, statistics, economics, and investment issues. The "Warp" in the title refers to the nonlinear nature of investment instrument variations.

The table below shows the variation in the price of the Vanguard Long-Term Treasury Index Fund ETF (VGLT) from May 2019 to April 2020, which was a period where the Fed reduced its federal funds rate from 2.39% to 0.05%. The S&P 500 crashed during this period.

As you can see, an investment in the VGLT early in that period would have appreciated about 31% at the end of the period. The VGLT is one of the lowest cost ETFs investing in long treasuries. This would have made purchasing VGLT shares analogous to buying “no expiration puts” on the S&P 500, with an extra advantage – the VGLT shares paid an interest.

The video linked below provides a brief discussion on these a few other related issues. Disclosure: the author owns VGLT shares at the time of this writing.

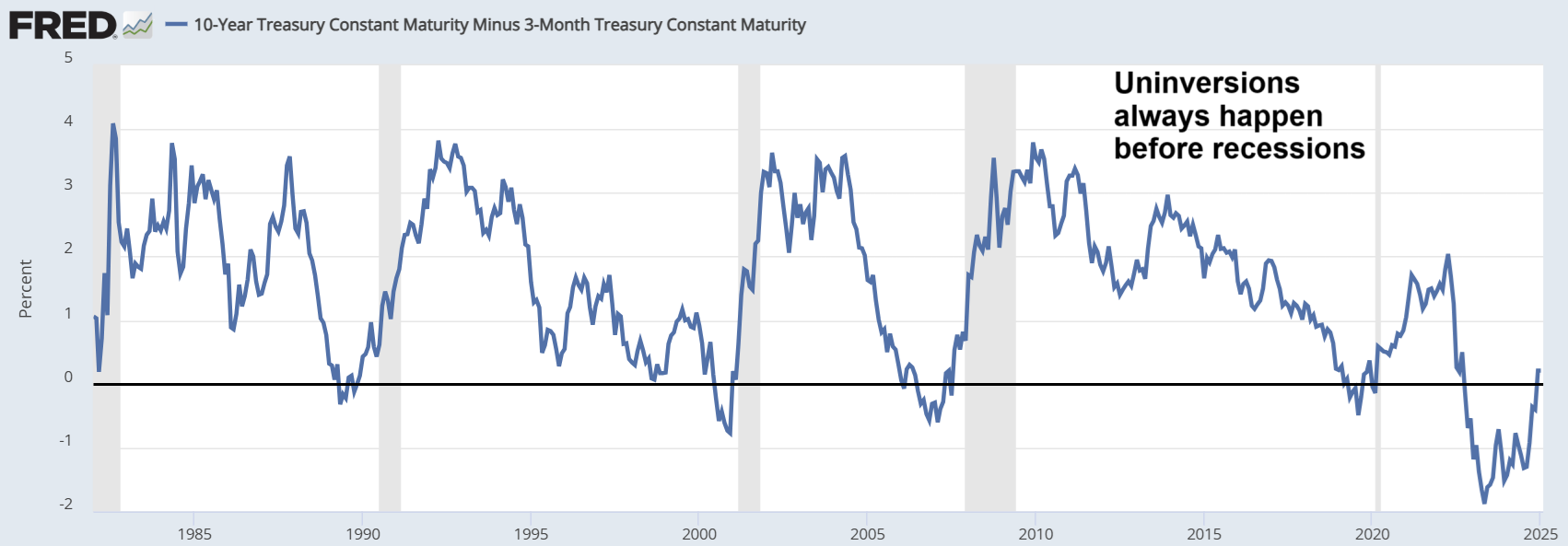

The figure below shows the graph of the 10y-3m Treasury yields for the period going from the early 1980s to 2025. The inversion in the 10y-3m graph is the best indication of an impending economic recession in the US, and that graph uninverts immediately prior to a recession.

As you can see, the uninversion of the 10y-3m Treasury yield curve is here, and universions always happen before recessions. Interestingly, this is happening at a time when many aspects of the US economy look strong. The video linked below provides a brief discussion on this a few other related issues.

The figure below shows five values of the TLT exchange-traded fund, which tracks the value of Treasury bonds with maturities of 20 years or more (i.e., long Treasuries), and of the corresponding 10-year Treasury yields. The latter, 10-year Treasury yields, are highly correlated, in a lagged way, with the Federal Funds rate. This rate is set by the Fed.

As you can see from the best fitting line equation, there is an increase of approximately 19 points in the value of the TLT for each 1% decrease in the 10-year Treasury yields. So, if the Federal Funds rate us expected to go down, the gain likely to be obtained by investing in long Treasuries in quite attractive. The video linked below provides a brief discussion on this a few other related issues.

The figures below show the graphs of the 10y-3m Treasury yields and 10y-2y Treasury yields. The inversion in the 10y-3m graph is the best indication of an impending recession, and that graph typically un-inverts immediately prior to a recession.

While the first graph does not show an un-inversion, the second (i.e., 10y-2y) does. And the second tends to predict the first, because the 2y yields tend to predict the 3m yields. That is where the yield curve un-inversion is, at the moment. The video linked below discusses this in a bit more detail.

Let us say that a coincidence involving two events, where one seems to predict the other, happens a number of times. How many times until it can be considered not only a coincidence, but a statistically significant pattern? We propose a framework to answer this question. Using the framework, we find that the number of times required is 7. We illustrate the practical application of our framework in the context of a very important phenomenon: When the percentage difference between 10-year and 3-month U.S. Treasury yields falls below zero, a U.S. recession appears to occur within the next 18 months.

All of this is laid out in much more detail in the article linked below. In this article, we have established the minimum number of times required for the inversion-recession phenomenon to be deemed more than a coincidence, and rather a statistically significant pattern. That number is 7. Therefore, given that since 1970 we have observed 8 instances of the inversion-recession phenomenon, we can conclude that this not a coincidence, and that it is in fact a statistically significant pattern.

The figure below shows two main graphs. The graph at the top shows the Fed funds rate from 1978 to 1987, approximately the period in which Paul Volcker served as Chair of the Federal Reserve. Rate hikes preceded the 1980 recession. Rates were raised again around 1981, then reduced, and then raised again; leading to the 1981-1982 recession.

The graph at the bottom shows the U.S. 10 Year Treasury yield, the CPI inflation rate (left scale), and the value of the S&P 500 index (right scale). Note that the U.S. 10 Year Treasury yield generally followed the Fed funds rate in the period, and that both were high while CPI inflation was still within approximately two-thirds of its previous peak. Interestingly, the S&P 500 was mostly flat during this period of major turmoil.

Could one conclude that the Fed’s current hiking cycle to combat inflation may have a similar outcome – i.e., a period where the S&P 500 is mostly range-bound? While it is possible that the answer to this question is “yes”, there is a big difference between today and the 1980s, namely valuations. The figures below show the valuations in the 1980s and now.

As you can see, valuations in the 1980s during the two recessions were largely below 10, whether we look at the S&P 500 PE ratio or the corresponding inflation-adjusted Shiller PE10 ratio. Today they are slightly above 20 (PE ratio) and 27 (PE10 ratio). The video linked below discusses these and related issues, as well as some recent developments.

The figure below shows two simulation-based valuations of the S&P 500. They assume a fair price-to-earnings (PE) ratio for the S&P 500 that is the inverse of half of the 10-year U.S. Treasury yield. The price (at the top) is the most recent top value of the S&P 500.

The numbers on the left consider a more benign scenario: S&P 500 earnings in 2023 are up by 4.70% from the previous year, and the 10-year U.S. Treasury yield is at 3.73%. The numbers on the right refer to a less positive scenario: S&P 500 earnings are up by 4.70%, and the 10-year U.S. Treasury yield is at 4.30%.

The second scenario takes us to a fair price for the S&P 500 of 2,537.50, which is 47.34% down from the most recent high. The video linked below discusses these simulations, some of the most recent values for the simulation inputs, and a few other things.

The figure below shows two simulation-based valuations of the S&P 500. They assume a fair price-to-earnings (PE) ratio for the S&P 500 that is the inverse of half of the 10-year U.S. Treasury yield. The price (at the top) is the most recent top value of the S&P 500.

The numbers on the left consider a rather benign scenario: S&P 500 earnings in 2023 are up by 4.70% from the previous year, and the 10-year U.S. Treasury yield is at 3.49%. The numbers on the right refer to a more likely scenario: S&P 500 earnings are up by 4.70%, and the 10-year U.S. Treasury yield is at 4.22%.

The second scenario takes us to a fair price for the S&P 500 of 2,667.12, which is 44.65% down from the most recent high. The video linked below discusses these simulations, some of the most recent values for the simulation inputs, and a few other options.

The figure below shows two simulation-based valuations of the S&P 500. They assume a fair price-to-earnings (PE) ratio for the S&P 500 that is the inverse of half of the 10-year U.S. Treasury yield. The price (at the top) is the most recent top value of the S&P 500.

The numbers on the left consider a rather benign scenario: S&P 500 earnings in 2022 are up by 5.60% from the previous year, and the 10-year U.S. Treasury yield is at 3.75%. The numbers on the right refer to a more likely scenario: S&P 500 earnings are up by 3.10%, and the 10-year U.S. Treasury yield is at 4.00%.

The second scenario takes us to a fair price for the S&P 500 of 2,644.39, which is 45.12% down from the most recent high. The video linked below discusses these simulations, some of the most recent values for the simulation inputs, and a few other options.

The figure below shows two simulation-based valuations of the S&P 500. They assume a fair price-to-earnings (PE) ratio for the S&P 500 that is the inverse of half of the 10-year U.S. Treasury yield. The price (at the top) is the most recent top value of the S&P 500.

The numbers on the left consider a rather benign scenario: S&P 500 earnings in 2022 are up by 10% from the previous year, and the 10-year U.S. Treasury yield is at 3.00%. The numbers on the right refer to a more likely scenario: S&P 500 earnings are up by 5%, and the 10-year U.S. Treasury yield is at 4.00%.

The second scenario takes us to a fair price for the S&P 500 of 2,693.12, which is 44.11% down from the most recent high. The video linked below discusses these simulations, some of the most recent values for the simulation inputs, and a few other options.

The figure below shows two simulation-based valuations of the S&P 500. They assume a fair price-to-earnings (PE) ratio for the S&P 500 that is the inverse of half of the 10-year U.S. Treasury yield. The price (at the top) is the most recent top value of the S&P 500.

The numbers on the left consider a rather benign scenario: S&P 500 earnings in 2022 are up by 10% from the previous year, and the 10-year U.S. Treasury yield is at 2.50%. The numbers on the right refer to a more likely scenario: S&P 500 earnings are down by 10%, and the 10-year U.S. Treasury yield is at 3.50%.

The second scenario takes us to a fair price for the S&P 500 of 2,638.16, which is 45.25% down from the most recent high. A sobering thought, given the rally that we are in right now, which many believe to be nothing more than another bear market rally.